A framework for thinking about global exposure

Related links

No related links

A helpful way to approach global allocation is to work through four simple, planning‑led questions.

The first is where the client expects to spend their money.

Clients who expect to fund their lifestyle predominantly in South Africa will naturally need a meaningful portion of their assets aligned to local conditions. Clients with global spending needs and liabilities or long‑term legacy objectives may benefit from greater exposure to global assets. Global investing is most effective when it reflects the currency of future spending, rather than being driven by fear or headlines.

The second question is when the money will be needed.

Time horizon plays a critical role in how global exposure behaves. Over short periods, currency volatility can have an outsized impact on outcomes. Over longer periods, global assets have historically added meaningful diversification and growth potential. Simply put, global investing tends to work more smoothly when time, rather than timing, is on the investor’s side.

The third consideration is client behaviour.

Clients do not experience portfolios as long‑term averages, they experience them through drawdowns and periods of stress. Global exposure introduces different patterns of volatility, and it is important that allocations reflect what clients can realistically tolerate without being forced into poor decisions at the wrong time.

Finally, advisers need to consider the investment wrapper.

Retirement funds, living annuities and discretionary investments each place different constraints on global exposure and carry different sequencing risks. It is entirely appropriate for the same client to have different global allocations across different vehicles (investment wrappers).

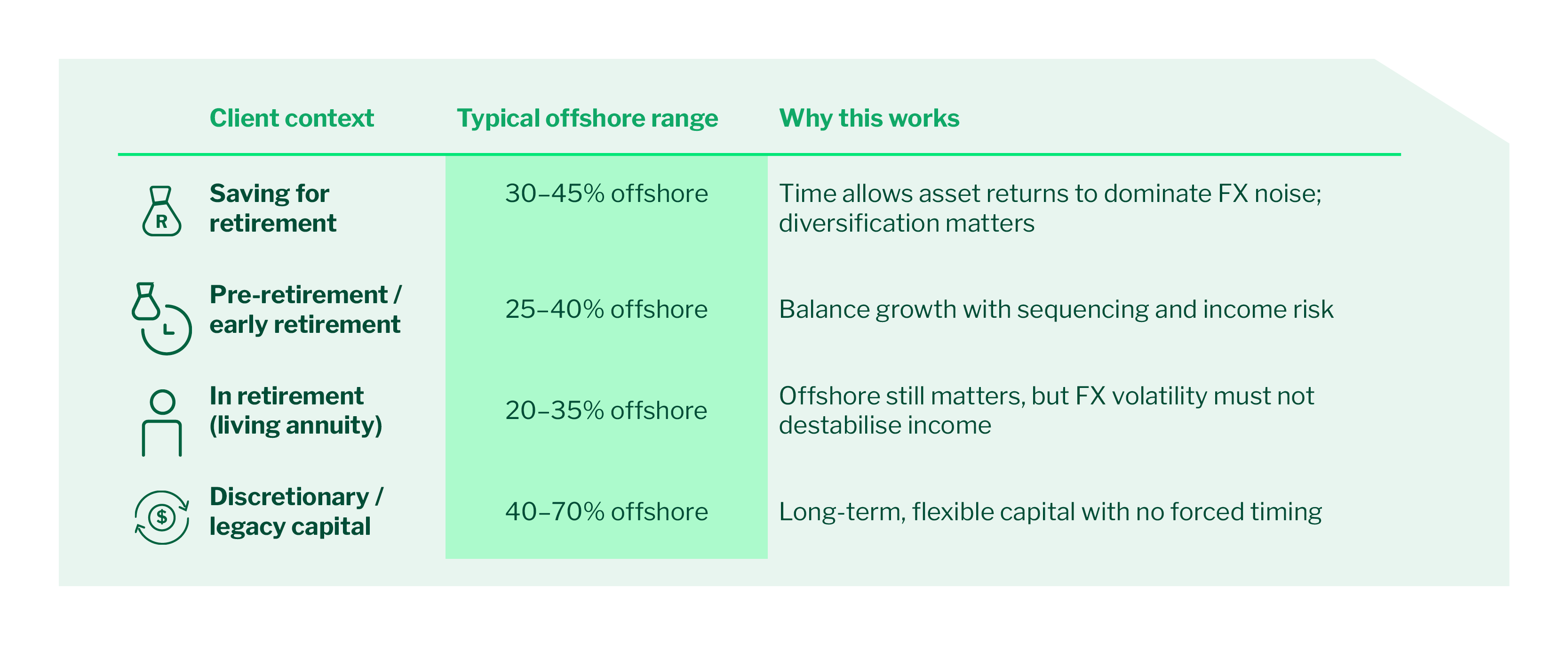

Moving from theory to sensible ranges

While there is no single global investment percentage that suits everyone, experience suggests there are broad ranges that tend to work well when aligned with purpose and time horizon. Long‑term retirement savers can typically accommodate higher global exposure than clients drawing income. Discretionary and legacy capital, with no forced timing, often allows for the greatest flexibility.

What matters most is not landing on a perfect number, but ensuring the chosen allocation is reasonable, defensible and aligned with the client’s circumstances. When that is the case, advisers do not need to be exactly right, they simply need to avoid being badly wrong.

A closing thought

Global investing works best when it is treated as a long-term design choice, not a short-term trade. When global exposure is aligned to purpose, time horizon and behaviour, and implemented through well structured multi asset solutions, it becomes a source of resilience rather than uncertainty.